SMM July 11th News:

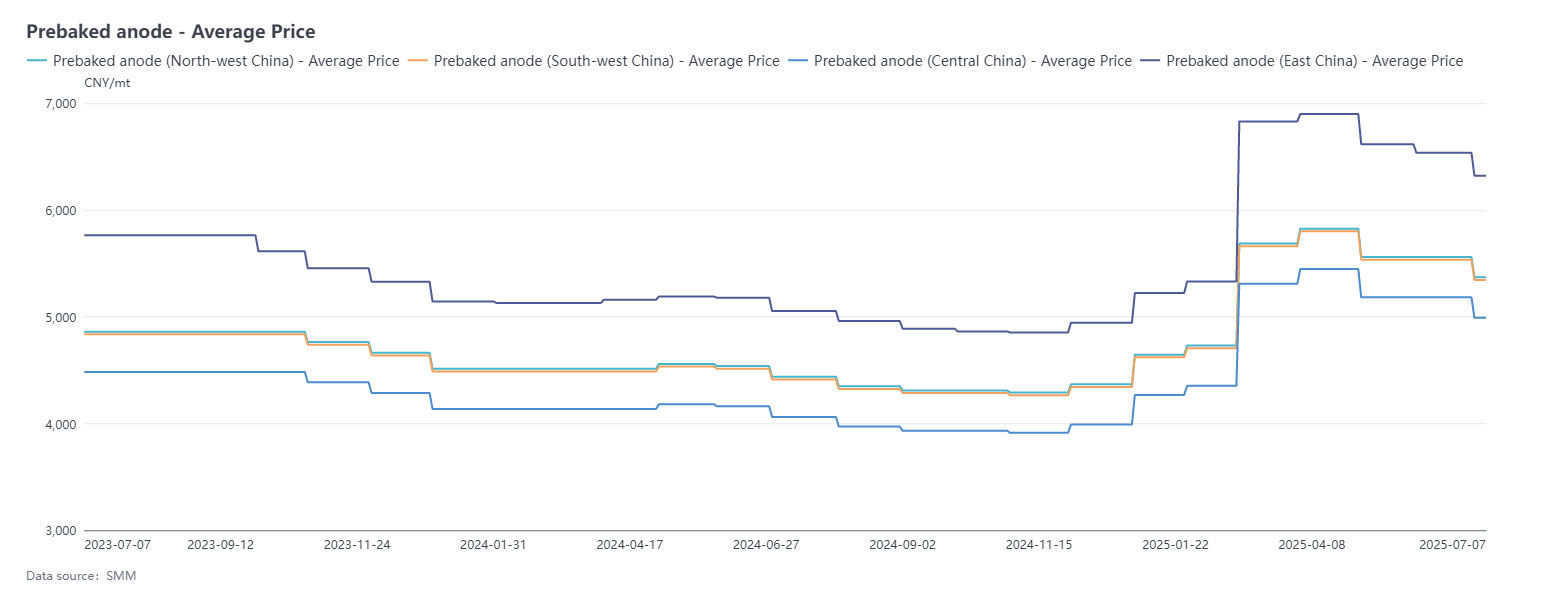

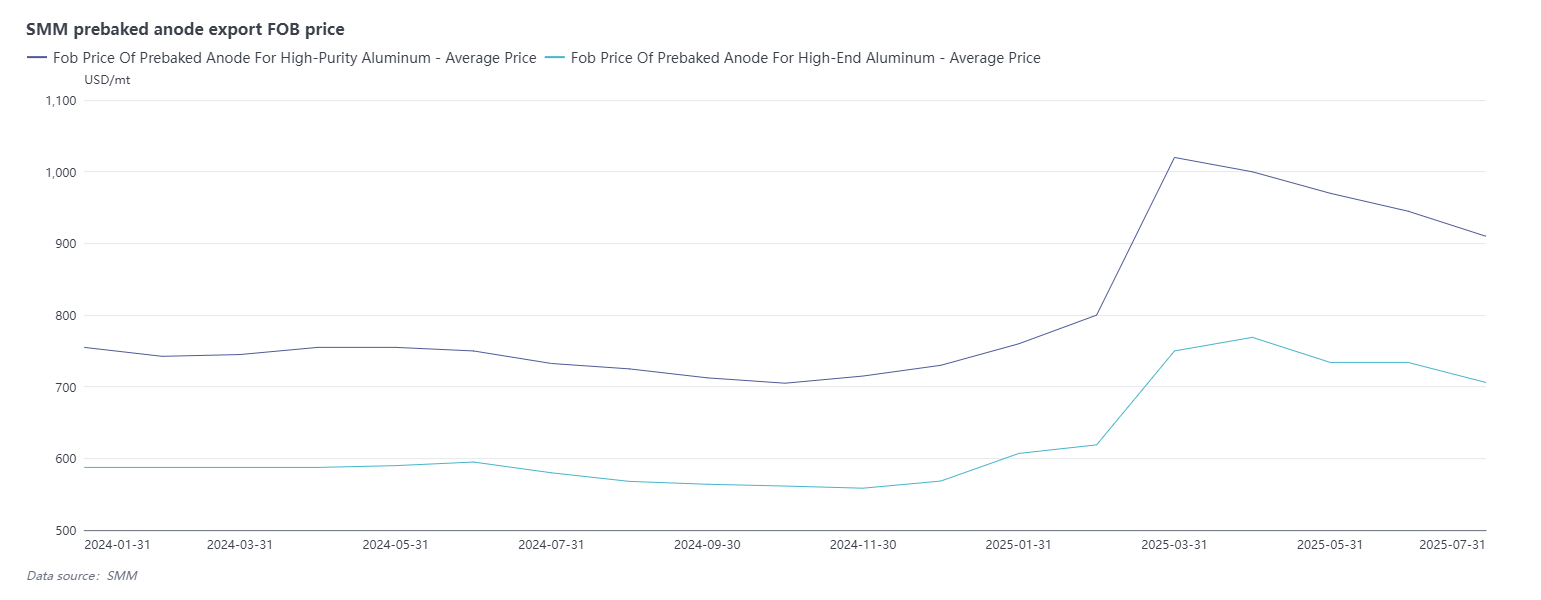

From June 6th to July 7th, SMM's prebaked anode prices continued to decline. The benchmark procurement price for an aluminum plant in Shandong for July 2025 was 4,749 yuan/mt, down 3.85% from the previous month's benchmark. According to SMM, the export order prices for prebaked anodes in July were mainly adjusted downward due to falling costs, with adjustments concentrated around $30-40/mt. As of now, SMM's anode prices in east China closed at 4,749-7,894 yuan/mt.

Raw Material Side: During this period, the market performances of petroleum coke and coal tar pitch diverged. For petroleum coke, the demand for stockpiling and restocking in the anode material market drove an improvement in overall refinery shipments for low-sulphur petroleum coke. Additionally, with maintenance plans at individual refineries in the north-east China region, expectations for a reduction in supply emerged, leading to a halt in the decline and a subsequent increase in low-sulphur coke prices. According to SMM statistics, as of now, the average price of low-sulphur coke in the north-east China region is approximately 3,667 yuan/mt, up 6.82% from June 6th. Local refinery petroleum coke prices continued to fall until mid-June due to poor downstream purchasing enthusiasm. However, as low-sulphur coke prices rebounded, downstream enterprises' enthusiasm for entering the market increased, refinery shipments improved, and petroleum coke prices adjusted upward in response to market conditions. Entering July, as petroleum coke prices rebounded to high levels and downstream enterprises' demand for stockpiling and restocking decreased, refinery shipment rates slowed significantly, and the upward momentum for petroleum coke prices continued to weaken. It is expected that petroleum coke prices will remain generally stable with a slight fall in the short term. As of July 7th, the average price of petroleum coke at SMM's local refineries was 2,240 yuan/mt, down approximately 2.35% from June 6th. In the coal tar pitch market, deep-processing enterprises operated at high capacity during this period, with relatively sufficient supply on the supply side. However, downstream demand was poor, leading to a continuous decline in coal tar pitch prices. According to SMM data, as of July 7th, the average price of coal tar pitch was 3,517 yuan/mt, down 12% from June 6th. Overall, cost support for prebaked anodes still exists.

Supply Side: Prebaked anode enterprises typically produce according to orders. In June 2025, the overall operating rates of domestic prebaked anode enterprises were mainly stable. From the perspective of capacity release, some enterprises resumed normal production after maintenance ended, leading to a rebound in production. A few enterprises upgraded their production efficiency through technological transformations, further driving production growth. The successful commissioning of the baking process for new projects in south-west China significantly increased the order volume for prebaked anode green blocks in the region, enhancing supply capability simultaneously. At the same time, the industry also faces pressure for periodic adjustments. Affected by the transfer of electrolytic aluminum capacity from Shandong to Yunnan, some local prebaked anode enterprises experienced a slight decline in production due to reduced supporting orders. In north China, stricter environmental protection inspections led to production constraints at individual enterprises, resulting in a periodic contraction in production. Additionally, June had one fewer production day compared to the previous month, which formed a certain inhibition on the industry's overall output. According to SMM data, the industry's operating rate in June was 75.84%, down 2.42 percentage points MoM. Supported by good order performance both domestically and overseas, the prebaked anode industry operated at a high level, and it is expected that the market supply of prebaked anodes will increase slightly in July. From a demand perspective, China's current operating capacity for electrolytic aluminum remains at a high level. Constrained by the capacity replacement policy, electrolytic aluminum capacity in Shandong is being transferred to Yunnan. Enterprises must complete production cut verification at their original plants before initiating construction of new facilities. This process led to a slight MoM decline in the operating rate of the electrolytic aluminum industry in June. Entering July, with the smooth commissioning of the second batch of capacity replacement projects in Yunnan, the industry's operating rate has shown a rebound trend, and there has been a regional adjustment in the domestic demand for prebaked anodes. In terms of export orders, prebaked anode export orders in 2025 have generally performed well, primarily due to the continuous release of new capacity in overseas electrolytic aluminum markets and the gradual recovery of production capacity in some enterprises. Based on prebaked anode export data for May 2025, exports have shown a MoM growth trend. Specifically, orders exported to Indonesia, Canada, and the UAE have seen significant increases, all exceeding 10%, with a total growth exceeding 80,000 mt. However, orders exported to Malaysia, Iceland, and Russia have declined. According to current customs data, SMM statistics show that China's cumulative prebaked anode export volume in 2025 reached 923,500 mt, up 9.08% YoY. Southeast Asia and the Middle East have become the core engines driving export growth due to industrial policy support and active investment, while some traditional markets have experienced demand contraction due to local capacity adjustments. Overall, prebaked anode export orders in 2025 have generally performed well, primarily due to the continuous release of new capacity in overseas electrolytic aluminum markets and the gradual recovery of production capacity in some enterprises. This trend has driven the growth of overseas market demand for prebaked anodes. Overall, the prebaked anode market in 2025 has demonstrated strong growth resilience, supported by dual demand from domestic and overseas markets.

Brief Commentary: During the period, a certain electrolytic aluminum enterprise in Shandong has adjusted the benchmark tender price for prebaked anodes in July 2025, with a MoM decrease of 190 yuan/mt. Meanwhile, a large domestic prebaked anode sales company has also synchronously reduced its sales pricing, with a MoM decrease of 239 yuan/mt. The petroleum coke market for raw materials has experienced significant fluctuations during the period, but the overall price center has risen, providing some support for prebaked anode costs. According to SMM data, as of July 7, the comprehensive cost of prebaked anodes in China has decreased to 4,748 yuan/mt, an increase of 1.67% from June 6. Although prebaked anode prices in July are expected to decline, the decline is smaller than anticipated, leaving some room for enterprise profitability. If calculated based on a one-month production cycle, the profitability of the prebaked anode industry continues to improve, with a theoretical MoM profitability improvement of approximately 70 yuan/mt. Most prebaked anode enterprises are in a state of marginal profitability. Entering July, the low-sulphur petroleum coke market continues to show a slight upward trend, while the upward momentum in the medium- and high-sulphur petroleum coke markets is significantly insufficient. According to SMM, this round of price increases is mainly supported by changes in downstream enterprises' purchasing sentiment, particularly the stockpiling in the anode material market, which has rapidly boosted market sentiment. However, there has been no significant improvement in actual downstream demand. Therefore, as subsequent sentiment gradually cools, there may be a risk of high-level price corrections for petroleum coke. Considering the above factors, SMM predicts that prebaked anode prices will remain in the doldrums next month.

Limited cost support led to a continuous decline in prebaked anode prices in July, with the transfer of aluminum electrolysis capacity reshaping the regional supply-demand pattern [SMM analysis]

During the period, a certain electrolytic aluminum enterprise in Shandong has adjusted the benchmark tender price for prebaked anodes in July 2025, with a MoM decrease of 190 yuan/mt. Meanwhile, a large domestic prebaked anode sales company has also synchronously reduced its sales pricing, with a MoM decrease of 239 yuan/mt. The petroleum coke market for raw materials has experienced significant fluctuations during the period, but the overall price center has risen, providing some support for prebaked anode costs. According to SMM data, as of July 7, the comprehensive cost of prebaked anodes in China has decreased to 4,748 yuan/mt, an increase of 1.67% from June 6. Although prebaked anode prices in July are expected to decline, the decline is smaller than anticipated, leaving some room for enterprise profitability. If calculated based on a one-month production cycle, the profitability of the prebaked anode industry continues to improve, with a theoretical MoM profitability improvement of approximately 70 yuan/mt. Most prebaked anode enterprises are in a state of marginal profitability. Entering July, the low-sulphur petroleum coke market continues to show a slight upward trend, while the upward momentum in the medium- and high-sulphur petroleum coke markets is significantly insufficient. According to SMM, this round of price increases is mainly supported by changes in downstream enterprises' purchasing sentiment, particularly the stockpiling in the anode material market, which has rapidly boosted market sentiment. However, there has been no significant improvement in actual downstream demand. Therefore, as subsequent sentiment gradually cools, there may be a risk of high-level price corrections for petroleum coke. Considering the above factors, SMM predicts that prebaked anode prices will remain in the doldrums next month.

Data Source Statement: Except for publicly available information, all other data are processed by SMM based on publicly available information, market communication, and relying on SMM‘s internal database model. They are for reference only and do not constitute decision-making recommendations.

For any inquiries or to learn more information, please contact: lemonzhao@smm.cn

For more information on how to access our research reports, please contact:service.en@smm.cn

Related News

![Middle East Geopolitical Risks Ease Significantly; Aluminum Prices Expected to Hover at Highs in the Short Term [SMM Aluminum Morning Meeting Minutes]](https://imgqn.smm.cn/usercenter/xHjXs20251217171650.jpg)

3 hours ago

Middle East Geopolitical Risks Ease Significantly; Aluminum Prices Expected to Hover at Highs in the Short Term [SMM Aluminum Morning Meeting Minutes]

Read More

Middle East Geopolitical Risks Ease Significantly; Aluminum Prices Expected to Hover at Highs in the Short Term [SMM Aluminum Morning Meeting Minutes]

[SMM Aluminum Morning Meeting Minutes: Geopolitical Risks in the Middle East Cool Significantly; Aluminum Prices to Fluctuate at Highs in the Short Term] Overall, from a macro perspective, easing geopolitical risks and the continued buildup of domestic social inventory have created bearish pressure on aluminum prices. However, the geopolitical situation in the Middle East remains unclear; if the conflict persists, expectations for a tightening of global aluminum supply are strong, and aluminum prices still have solid upward momentum. In the short term, aluminum prices are still expected to hold up well.

3 hours ago

![Primary Aluminum Drove a Sharp Rally in Alloys, While the Raw Material Side Continued to Strengthen [SMM Cast Aluminum Alloy Morning Comment]](https://imgqn.smm.cn/usercenter/dKkIN20251217171654.jpg)

3 hours ago

Primary Aluminum Drove a Sharp Rally in Alloys, While the Raw Material Side Continued to Strengthen [SMM Cast Aluminum Alloy Morning Comment]

Read More

Primary Aluminum Drove a Sharp Rally in Alloys, While the Raw Material Side Continued to Strengthen [SMM Cast Aluminum Alloy Morning Comment]

[SMM Cast Aluminum Alloy Morning Comment: Prices Pull Back as Aluminum Scrap Holders Are Reluctant to Sell; Overall Market Trading Remains Muted] Yesterday, the SMM ADC12 price rose by 500 yuan/mt, with the center of market quotations moving up markedly. Most producers’ price adjustments were concentrated in the 500–600 yuan/mt range. Recently, raw material prices have continued to strengthen, and the cost side has risen quickly, providing a clear lift to enterprise quotations. However, downstream demand has been relatively steady. Most enterprises reported that orders and inquiry activity were generally average, and downstream purchasing remains mainly restocking on an as-needed basis. Supported by cost-driven momentum and market expectations, enterprises have shown a clear willingness to raise prices. In the short term, against the backdrop of cost support and mild supply release, ADC12 prices are expected to hold up well. The medium-term trend will still depend on the recovery of end-use consumption. If die-casting industry orders increase significantly, the price center is expected to move up further; if demand recovery falls short of expectations, coupled with a continued rise in operating rates on the supply side, prices will shift from elevated levels into rangebound consolidation.

3 hours ago

![Secondary Aluminum Operating Rate Plunged in February March Recovery Was Set to Rebound Significantly [SMM Analysis]](https://imgqn.smm.cn/production/admin/votes/imageskkgTu20240508153005.png)

19 hours ago

Secondary Aluminum Operating Rate Plunged in February March Recovery Was Set to Rebound Significantly [SMM Analysis]

Read More

Secondary Aluminum Operating Rate Plunged in February March Recovery Was Set to Rebound Significantly [SMM Analysis]

[SMM Analysis]Secondary Aluminum Operating Rate Plunged in February March Recovery Was Set to Rebound Significantly

19 hours ago

Related News

Middle East Geopolitical Risks Ease Significantly; Aluminum Prices Expected to Hover at Highs in the Short Term [SMM Aluminum Morning Meeting Minutes]

Mar 10, 2026 09:19

Primary Aluminum Drove a Sharp Rally in Alloys, While the Raw Material Side Continued to Strengthen [SMM Cast Aluminum Alloy Morning Comment]

Mar 10, 2026 09:09

Secondary Aluminum Operating Rate Plunged in February March Recovery Was Set to Rebound Significantly [SMM Analysis]

Mar 09, 2026 17:50

Data: SHFE, DCE market movement (Mar 09)

Mar 09, 2026 16:52